With 30 June fast approaching, it is time to review your superannuation position to see if there are any strategies that might benefit you. The superannuation environment is a great place to invest for your future. You can invest in all the same asset types you can utilise outside of superannuation while benefiting from the concessional (more generous) taxation rules that superannuation provides.

If you think that one or more of these options could be right for you, please contact us as soon as possible. While we have tried to make this summary as simple as possible, some of these strategies can be quite complicated or time-consuming to implement.

Tax Deductible Superannuation Contribution

From 1 July 2017, individuals eligible to make contributions to superannuation, have been able to claim an income tax deduction for personal superannuation contributions up to the concessional contribution cap of $25,000.

Remember that the $25,000 cap also includes your employer compulsory contributions.

If you have surplus cash available, you could make a concessional contribution to your superannuation fund and claim a deduction for the contribution in your tax return. The tax deduction lowers your taxable income and therefore your personal income tax liability. This could lower the amount of tax you need to pay or turn a tax bill into a tax refund.

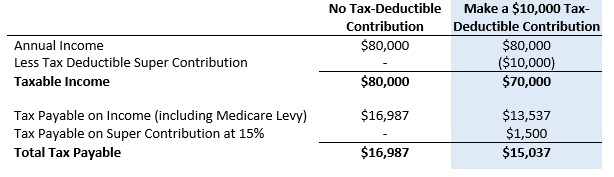

Please see the below example based on taxable income for the year of $80,000.

By making a $10,000 concessional contribution, this person has saved for their retirement, sheltered their funds from future taxes by moving funds them into the superannuation environment, and reduced their income tax payable by $1,950 ($16,987 – $15,037).

Catch Up Contribution

Since 1 July 2018, individuals with superannuation balances of less than $500,000 can make additional concessional contributions using any concessional contribution cap left unused since 1st July 2018.

This could be a good strategy if you made a capital gain this financial year and have unused contributions from 2018/2019 or 2019/2020.

Contribution Caps

There are limits to the amount you can contribute into superannuation per year. These caps are:

![]()

Non-concessional contributions are after-tax contributions such as spouse contributions and contributions made under the Super Co-Contribution Scheme. Non-concessional contributions were previously known as undeducted contributions.

Concessional contributions are before-tax contributions and include your employer’s compulsory contributions, additional employer contributions, and any amounts that you salary sacrifice into superannuation.

Superannuation Co-Contribution

Superannuation co-contributions help eligible people boost their retirement savings. If you are a low or middle-income earner and make an after-tax contribution to your super fund, the government may also make a contribution (called a co-contribution) up to a maximum amount of $500.

The eligibility criteria are as follows:

- Your total income is equal to or less than the lower threshold of $39,837 for the 2020/2021 financial year,

- At least 10% of your assessable income must come from either employment-related activities or carrying on a business,

- You will be younger than 71 years old at the end of the financial year, and

- You lodge a tax return.

If you satisfy the above criteria, a strong case can be made for a $1,000 contribution to your superannuation fund before 30 June 2021. The federal government will then also contribute to your account, to the effect of $500. This can be thought of as an immediate and guaranteed 50% return on your investment.

If your eligible income is above the lower threshold of $39,837 but below the upper threshold of $54,837 for the 2020/2021 financial year, and you satisfy the above criteria, you will be eligible for a reduced Government Co-Contribution.

You do not even need to apply for the super co-contribution. When you lodge your tax return, the ATO will determine if you are eligible. If the super fund has your tax file number (TFN) the payment will be made directly to your superannuation account.

Spouse Contribution

If you have a spouse who earns less than $37,000 and you make a spouse super contribution of up to $3,000, you can claim a personal tax offset of 18% of the contribution up to the maximum rebate of $540. The tax offset phases out when your spouse earns $40,000 or more.

Your spouse’s income includes their assessable income, reportable fringe benefits and any reportable employer super contributions such as salary sacrifice.

Non-Concessional Superannuation Contribution

Non-concessional contributions are super contributions made from your own after-tax monies. You do not claim a tax deduction for these contributions, and they are capped at $100,000 each year. You must be under 67, or if aged between 67 and 74, meet the work test to qualify. And your total super balance (as at 1 July 2020) must also be less than $1,600,000.

If you are under age 65 (or were as of 1st July 2020), then you can access the “bring-forward rule” which allows you to make up to three-years’ worth of contributions or $300,000 in one go. A couple could potentially contribute $600,000 into super. Ability to access this is further limited by your total super balance (under $1.4m full amount; $1.4m to $1.5m $200,000; $1.5m to $1.6m $100,000).

Superannuation is a tax effective investment vehicle, if you have surplus cash this may be a good strategy for you to consider especially in the lead up to retirement.

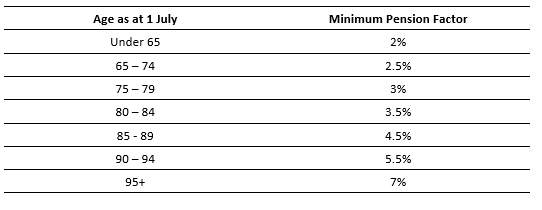

Minimum Pension Drawdown

You are required to drawdown a minimum amount of pension each year to satisfy legislative requirements. This amount must be withdrawn before 30 June.

The Government reduced the minimum pension drawdown for 2019/20 and 2020/21 to assist retirees following the Covid-19 pandemic. The minimum drawdown factor is determined by your age and is calculated each year. The table below illustrates the reduced minimum pension factors for each age group for the 2020/2021 financial year: