JobMaker Hiring Credits: What We Know So Far

We’ve had quite a few questions about the JobMaker hiring credit announced in the 2020-21 Federal Budget. The legislation enabling the JobMaker scheme has not passed Parliament as yet and until this occurs, the JobMaker rules are not certain and may change. More details should be available soon and we’ll let you know as soon as we have some certainty. Here is what has been announced so far:

What is JobMaker?

JobMaker is a credit available to eligible businesses for hiring additional employees (not if you are merely replacing someone who left). The hiring credit is available for jobs created from 7 October 2020 until 6 October 2021.

The credit provides:

- $200 per week for new employees between 16 to 29 years of age, and

- $100 a week for new employees between 30 to 35 years of age.

Payment is from the start date of the employee for 12 months.

When do the credits start?

Assuming the legislation passes Parliament and your business and the employee are eligible, and the ‘additionality’ test is passed (see How can we access JobMaker), credits can be claimed for employees hired from 7 October 2020 until 6 October 2021. The credit will be claimed quarterly in arrears by the employer from the ATO from 1 February 2021. The credit is an incentive for the employer to support wage costs and not passed onto the employee.

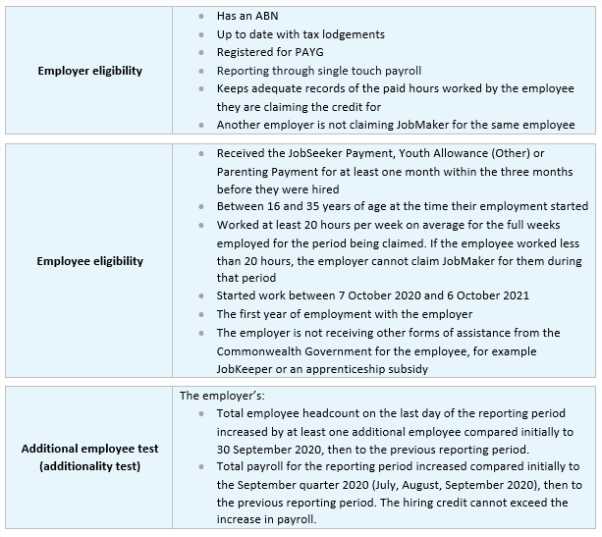

How can we access JobMaker?

There are three tests for JobMaker:

Government entities or agencies, banks and other institutions subject to the bank levy, businesses in liquidation, and foreign Government entities (unless a resident entity), are unable to access JobMaker.

I can only claim JobMaker if the number of employees and payroll increases. What happens if one of my team resign? Through no fault of the business?

Your business can only receive JobMaker for your eligible employees if total employee headcount and payroll increases. If the headcount or payroll decreases or remains the same, JobMaker cannot be claimed for that period.

For example, if you had three staff at September 2020 and hired an additional two employees in late October 2020, your business can claim JobMaker for the two new employees assuming the business and the employer are eligible and payroll has increased compared to the September 2020 quarter. However, in December 2020, one of your original staff members resigns. As a result, your business can only claim JobMaker for one eligible employee in December as your headcount has increased by one, not two, compared to the September 2020 baseline.

A similar baseline concept applies to payroll. If you employed new eligible employees in October 2020 but your overall payroll remained the same or only increased marginally because the hours of your existing staff reduced when the two new employees were employed, then the JobMaker credit will only be the additional payroll amount. That is, if the JobMaker credit for the two employees for the quarter is $8,960, but payroll compared to the September 2020 quarter only increased by $1,200, then the JobMaker credit you receive would be $1,200. The JobMaker credit cannot exceed the increase in payroll.

Each month, employers will need to ensure they pass these ‘additionality’ tests before claiming.

Your headcount and payroll increase is measured on the last day of each reporting period from the date your first new employee started. For example, if your first new employee joined in October 2020, your baseline is set at that point. If a new employee starts in January 2021, your payroll and headcount baseline is measured from the last reporting period, in this case, December 2020 for headcount and the December quarter for payroll. That is, your baseline commences from the date your new employee starts and then is reassessed each reporting period to ensure there is an increase.

If I don’t hire new staff until January 2021, can I claim JobMaker for 12 months or only up to 6 October 2021?

JobMaker is available for 12 months for eligible employees hired from 7 October 2020 until 6 October 2021. If you hire new employees from January 2021, JobMaker is available for 12 months for these employees assuming that the employees and business are eligible and the ‘additionality’ test is passed.

The baseline for the ‘additionality’ tests – headcount and payroll – starts from the start date of your new employee. The Government has indicated that the baseline for the ‘additionality’ test will be adjusted in the second year of the program to ensure an employer can only receive JobMaker for 12 months for each additional position created. The detail of exactly how these rules will work has not been released as yet.

My business did not have employees in September but I hired my first employee in late October. Can I claim the JobMaker credit for them?

Businesses with no employees on 30 September, cannot claim JobMaker for their first employee. However, JobMaker can be claimed for your second and any subsequent employees that started on or before 6 October 2021.

Can the business get JobKeeper and JobMaker?

No. Once your business exits JobKeeper and is no longer receiving JobKeeper payments for any employees or business participants, if eligible, the business could then start to receive JobMaker credits. The business is eligible for the hiring credit in the reporting period following your JobKeeper exit date.

The JobMaker credit and the details of how the rules will apply are subject to change. Please do not make decisions based on the JobMaker information available as the final shape of the legislation could change. We will provide a summary of the rules and how you can claim the JobMaker hiring credit as soon as the rules are confirmed.

Tax deductions for investing in your business

Stimulating investment is high on the Government’s agenda. To encourage spending, the 2020-21 Budget introduced a measure that allows businesses with turnover under $5bn* to immediately deduct the cost of new depreciable assets and the cost of improvements to existing assets in the first year of use. This means that an asset’s cost will be fully deductible in the year it’s installed ready for use, rather than being claimed over the asset’s life. And, there is no cap on the cost of the asset.

When it comes to second-hand assets the rules are a bit different depending on the size of the business. Businesses with an aggregated turnover under $50 million can claim an immediate deduction for the cost of second-hand assets under the new measures.

Businesses with aggregated annual turnover between $50 million and $500 million can still deduct the full cost of eligible second-hand assets costing less than $150,000 that are purchased by 31 December 2020 under the existing enhanced instant asset write-off. Businesses that hold assets eligible for the enhanced $150,000 instant asset write-off will have an extra six months, until 30 June 2021, to first use or install those assets.

For small business entities that have assets in a general pool the changes seek to ensure that pool balances are completely written-off for tax purposes in the 2021 and 2022 income years.

These super-charged immediate deduction rules tie into the existing instant asset write-off for businesses with a turnover under $500 million (summarised below).

The instant asset write-off only applies to certain depreciable assets. There are some assets, like horticultural plants, capital works (building construction costs, etc.) and certain intangible assets that don’t qualify for the new rules.

If your business will make a tax profit this year, this measure is likely to reduce the taxable income of the business for the year and it may be possible to vary upcoming PAYG instalments to improve cash flow. If your business operates through a company and will make a tax loss, you might be able to use the loss to offset tax paid in previous years (see Refunds for Tax Losses). Alternatively, tax losses can generally be carried forward to a future year.

Refunds for Tax Losses

If your company has made a loss, you may be able to claim a tax refund for tax previously paid on profits.

In the 2020-21 Federal Budget, the Government announced that businesses with turnover under $5bn* will be able to offset any losses made between 2019-20 and 2021-22 against previously taxed profits between 2018-19 and 2020-21.

The loss carry-back rules enable a company to offset tax losses against profits taxed in a previous year, generating a refundable tax offset. The amount carried back can be no more than the earlier taxed profits, limiting the refund to the company’s tax liabilities in the profitable years. The company can choose to carry-back a loss or carry it forward. That is, tax losses for the 2019-20, 2020-21 or 2021-22 income years can either be:

- Carried forward and deducted against income derived in later income years; or

- Carried back against income of earlier income years as far back as the 2018-19 income year to produce a refundable tax offset.

Previously, tax losses could only be carried forward and deducted against income in later income years.

This is not the first time that carry-back losses have been allowed. The loss carry-back rules were introduced some years ago by the Gillard government for the 2012-13 year, then repealed.

The loss carry-back rules also interact with the Government’s Budget measure allowing immediate expensing of investments in capital assets (See Tax deductions for investing in your business). The new investment will generate significant tax losses in some cases which can then be carried back to generate cash refunds for eligible companies.

What entities are eligible to carry-back losses?

Corporate tax entities are eligible to carry-back losses – a company, a corporate limited partnership, or a public trading trust – BUT only if the entity has lodged an income tax return for the current year and each of the five years immediately preceding it. If your company has not kept up to date with its reporting obligations, it might not be able to use the new rules.

Claiming the refundable tax offset

Businesses will need to elect to utilise their carry-back losses when they lodge their 2020-21 and 2021-22 tax returns. That is, even if the company made a loss in the 2019-20 year, it cannot claim that loss until the 2020-21 tax return is lodged.

For the 2020-21 income year, a loss carry-back tax offset may be available to a company if:

- It has a tax loss in the 2019-20 income year and/or the 2020-21 income year;

- It has an income tax liability in the 2018-19 income year and/or the 2019-20 income year; and

- For the 2020-21 income year and each of the previous five income years, either the entity has lodged an income tax return; the entity was not required to lodge a return; or the Commissioner has made an assessment of the entity’s income tax.

The carry-back cannot generate a franking account deficit. That is, the refund is further limited by the company’s franking account balance.

The 2020-21 Budget delivered a range of incentives for business to invest. If you would like us to review your position and the tax impact of any investments you are contemplating, please call us and we can assist you to get the best possible outcome.

*Aggregated turnover. Aggregated turnover is your turnover plus the annual turnover of any business connected with you or that is your affiliate.

Tax table reminder

The 2020-21 personal income tax cuts announced in the Federal are now law. Employers need to ensure that the tax withheld from employee salaries is correct. The ATO has published updated tax tables that apply from 13 October 2020. Employers have until 16 November 2020 to implement the changes.

JobKeeper clawback begins

At the recent Senate Estimates hearing, Jeremy Hirschhorn, the ATO’s Second Commissioner, stated that $120 million in JobKeeper payments had been clawed back from those either deliberately seeking to rort the system or who had made reckless mistakes. Mr Hirschhorn went on to say that there did not appear to be widespread fraud across the Government’s stimulus measures and most mistakes were honest. In the cases identified so far, JobKeeper had not been clawed back from employers making honest mistakes but these employers were prevented from making future claims.

In September, the ATO noted that compliance checks had halted 55,000 JobKeeper applications at the very first stage, because they did not meet the eligibility criteria, and delayed $1bn in payments to more than 75,000 applicants for further review. Eleven matters have been referred to Serious Financial Crime Taskforce operations and around 50 matters referred for criminal investigation. But overall, the Tax Commissioner stated, “the vast majority of Australians have done the right thing and only claimed the amounts they were entitled to.”

APRA reveals $34.4bn super early release

Over $34.4bn has been released from Australian Superannuation Funds under the COVID-19 early release scheme, the Australian Prudential Regulation Authority revealed. The figures, which do not include self-managed super funds, show the deep impact of the scheme on superannuation balances. 3.3 million initial applications and 1.3 million subsequent applications were received by funds.